Journal of Financial Planning: May 2017

Jamie Patrick Hopkins, J.D., LL.M., RICP®, ChFC®, CLU®, holds the Larry R. Pike Chair in Insurance and Investments at The American College of Financial Services and is an associate professor of taxation and co-director of The American College New York Life Center for Retirement Income in Bryn Mawr, Pa.

Executive Summary

- This article is designed to help financial advisers better understand the potential knowledge level and desires of their clients with regard to reverse mortgages and home equity as a retirement income source.

- Results of a 2016 survey of 1,000 Americans ages 55 to 75 are discussed, including attitudes toward home equity and retirement planning with a special focus on reverse mortgages.

- Survey respondents were quizzed on their reverse mortgage literacy; they performed poorly with an average score of 48 percent.

- The existence of a relationship with a financial adviser did not increase the likelihood the respondents would consider a reverse mortgage, nor did it increase their reverse mortgage knowledge.

- Overall, respondents did not have a positive view of reverse mortgages as a retirement income tool. Low literacy rates and negative opinions regarding reverse mortgages appear to be restricting wider usage of the product.

For the average american couple at age 65, home equity makes up more than two-thirds of their total wealth, according to 2011 U.S. Census data. More specifically, the median net worth for married couples age 65 and older is $284,790. Of this amount, $192,552 is in home equity, and $92,238 is in non-equity assets, including IRAs, other savings, and personal property.

These asset values alone imply that retirees may be facing a retirement income shortfall. A 2016 Bankrate study1 found that in 47 states the median income of individuals age 65 and older was less than 70 percent of pre-retirement income, a common benchmark for determining income adequacy. Studies focusing on future retirees have also found a substantial risk of a shortfall. EBRI’s Retirement Security Projection Model® shows that those ages 35 to 65 face a $4.13 trillion shortfall. However, when looking specifically at the early baby boomers who are at risk of the shortfall, the EBRI study showed the shortfall to be $71,299 per individual for married households, $93,576 for single males, and $104,821 for single females (VanDerhei 2015).

If many Americans who may be facing a retirement income shortfall have much more home equity than IRA or 401(k) savings, it seems that incorporating home equity into a retirement income plan would make sense. However, current data shows that this may not be the case. A 2016 Transamerica study2 found that of more than 2,000 American retirees, only 11 percent reported using home equity as a current source of retirement income.

Because retirement income planning is often goal-based and specific to each client, a variety of strategies can be used to tap into home equity to support a secure retirement. Homeowners can tap into home equity by: (1) selling the home and downsizing; (2) using a traditional home equity line of credit (HELOC); (3) entering into a sale-leaseback arrangement; (4) utilizing any special purpose loans made available in their state; (5) home sharing/renting out rooms; or (6) securing a reverse mortgage.

Considering Reverse Mortgages

While there are a variety of ways to use home equity as part of a retirement income plan, reverse mortgages deserve special consideration for many reasons. In part, reverse mortgages should be considered because many retirees remain in their home in retirement and need more retirement income. According to the U.S. Department of Health and Human Services, from 2014 to 2015, only 4 percent of individuals age 65 and older moved as opposed to 13 percent of the under-65 population. Approximately 60 percent of older movers stayed in the same county, and an additional 21 percent remained in the same state but in a different county. Only 20 percent of the movers moved out-of-state or abroad.3

Another reason to look at a reverse mortgage is that through the line of credit and other withdrawal options, a reverse mortgage can be accessed when the need arises and can be used to meet many retirement income objectives.

Many people have reservations about reverse mortgages. This can be seen in the data on the number of reverse mortgages initiated each year. In the fiscal year from October 1, 2015 to September 30, 2016, 48,902 Home Equity Conversion Mortgage (HECM) reverse mortgages were initiated. This number has been decreasing, with a peak in 2009 of 114,692, according to the National Reverse Mortgage Lenders Association.4

Although a few proprietary reverse mortgage options develop every few years, the HECM is the predominant reverse mortgage program in the United States (and therefore, this paper focused solely on the HECM program). The HECM is heavily regulated by the U.S. Department of Housing and Urban Development (HUD) and the Federal Housing Administration (FHA). The government has made frequent adjustments to the regulations and program over the past decade. In the past few years, the regulations have focused on streamlining the product to make it simpler and less expensive. Additionally, protections were added for non-borrowing spouses and a financial assessment is now required to ensure that any borrower will now be able to meet his or her other required home maintenance expenses during the course of the reverse mortgage.

There are reasons to be cautious with reverse mortgages. First, reverse mortgages can be expensive when compared to other forms of home loans such as traditional forward mortgages and HELOCs. Usually, borrowers roll the fees and closing costs directly into the loan. Because people rarely make monthly payments on the loan, the interest will accumulate over time and with this compounding interest the loan amount can rise quickly.

Furthermore, the upfront fees and total costs related to a reverse mortgage can be confusing. Fees and costs depend on how the reverse mortgage is used. In a cash-out refinance, the costs are very similar to a traditional FHA financing. Every loan is unique and dependent on what company the borrower goes through, but some general upfront costs are fairly consistent. HUD requires that origination fees cannot exceed 2 percent of the first $200,000 in home value and 1 percent of the home value over $200,000, with a hard cap of $6,000 (Hultquist 2017).

Additionally, the borrower will pay the initial mortgage insurance premiums, which will be a charge of 0.5 percent or 2.5 percent of the maximum claim amount, depending on the situation. The homeowner will also likely pay closing costs, settlement fees, title insurance, recording fees, and perhaps attorney costs. However, lenders will often offer credits to help offset some of the costs, and that can result in homeowners having upfront costs of less than 1 percent of the home value at the time of closing. In the end, reverse mortgages can be slightly more expensive than a traditional forward mortgage.

A reverse mortgage also has ongoing costs. Once the homeowner is carrying a balance, the compounding interest will kick in. Today, interest rates are around 4.75 percent plus a yearly ongoing 1.25 percent annual mortgage insurance cost. For example, if a homeowner has a $10,000 balance with a roughly 6 percent total rate today, the cost will be $600 to the borrower that year. Although the borrower could pay the interest, instead many borrowers roll it into the balance, creating a new balance of $10,600. The reccurring cost to the borrower also needs to be incorporated when determining the total cost structure of a reverse mortgage. It is also important to remember that any funds not distributed will grow at the same rate as the funds the borrower did draw.

The homeowner is still responsible for taxes, maintenance costs, and insurance on the home. As such, we have seen people foreclosed upon after they have spent the reverse mortgage money, leaving them without any additional home equity and without a home. Therefore, in the worst-case scenario, a reverse mortgage can be very expensive, complicated, and the borrower can end up spending all their home equity and losing their home.

Although risks exist with reverse mortgages, it remains a financial tool that is often misunderstood both by consumers and financial services professionals. Nobel Prize-winning economist Robert C. Merton, a finance professor at MIT’s Sloan School of Management, stated that Americans have wrongly steered clear of reverse mortgages (Blumenthal 2015). Several studies (discussed in the next sections) have shown the benefits of incorporating reverse mortgages in a retirement income plan, and financial advisers are gaining more exposure to reverse mortgages through education and designation programs that focus specifically on retirement income planning.

In this environment where reverse mortgages are gaining acceptance as a valuable retirement income tool by researchers and financial advisers, it is still curious to see the reluctance by consumers to use reverse mortgages. This study was designed to look at consumers’ attitudes toward using home equity in retirement and to test their knowledge specifically about reverse mortgages. The goal was to gain insight into consumer attitudes to better understand their current behavior and how to talk to and educate them about reverse mortgages.

Overview of the Study

The study consisted of an online survey conducted by Greenwald & Associates on behalf of The American College of Financial Services through the Research Now survey panel in the spring of 2016. The survey consisted of three sets of questions: (1) demographic; (2) attitudinal; and (3) knowledge checks. Some questions were scored on a Likert scale from 1 to 7, while others were yes or no questions. The literacy questions were True, False, and I Don’t Know.

The American College’s faculty created the survey’s knowledge check questions with input from 14 different reverse mortgage industry firms, organizations, and experts to ensure accuracy. The survey was completed by 1,003 people: 537 males and 466 females between the ages of 55 and 75 with at least $100,000 of investable assets and at least $100,000 in home equity. Renters were not surveyed.

The goal of the “Home Equity and Retirement Income Planning Survey” was to gauge the knowledge levels of those nearing or in retirement about reverse mortgages, to understand attitudes about the importance of housing decisions for those nearing or in retirement, and to find ways to help advisers incorporate home equity in their retirement income planning discussions.

Five main takeaways come from the survey results: (1) most of the survey respondents demonstrated a strong desire to age in place; (2) most of the respondents had not considered home equity as a part of their retirement plan; (3) only about 25 percent of respondents felt comfortable using home equity as an income source in retirement; (4) respondents showed a significant level of misconceptions about reverse mortgages, essentially failing the knowledge test with an average score of 48 percent; and (5) even respondents who wanted to live in place and felt comfortable using home equity as a retirement income option did not understand many of the basic features of reverse mortgages. Ultimately, there is a strong desire to age in place but most of the respondents do not understand nor do they seek strategic uses of home equity as a retirement income option.

The low literacy scores regarding reverse mortgages and the lack of home equity planning may be seen both as a cause for concern and a real opportunity for planners. With a growing body of research surrounding effective uses of home equity, a push toward more comprehensive planning, and the large amount of baby boomer home equity wealth, the financial planning community appears to be primed to incorporate the home into retirement income planning. However, this research did find that the existence of a financial adviser relationship had no significant impact on the client’s likelihood to have considered home equity as a retirement income source.

Literature Review

In addition to being able to age in place, access to home equity can be used in a variety of strategic ways to improve retirement, including: helping to build a bridge of income early in retirement to avoid taking Social Security prematurely; improving portfolio sustainability through reduced exposure to sequence of returns risk; managing cash flow; and generating tax-efficient retirement income to allow Roth conversions and manage taxes.

In response to an increased need to incorporate home equity into retirement income planning, some researchers have tested effective uses of reverse mortgages. Sacks and Sacks (2012) used Monte Carlo simulations to quantify how retirement spending strategies experienced higher probabilities of success when using a reverse mortgage early in retirement as opposed to a last resort. The research found that coordinating a reverse mortgage with investment portfolio withdrawals (by pulling income from the reverse mortgage in years that follow a negative return for the investment portfolio) helped improve the success rate of the portfolio and improved the possibility for leaving a legacy. The reason for the improvement in performance and legacy was that the home equity provided a non-market correlated income stream to help provide a cushion against sequence of returns risk.

Salter, Pfeiffer, and Evensky (2012) found significant benefits in coordinating a reverse mortgage line of credit with a systematic portfolio withdrawal strategy to generate retirement income. In the simulation, the coordinated reverse mortgage strategies had success rates between 78 and 82 percent, compared to 52 percent in the baseline strategy that did not use the reverse mortgage line of credit. Wagner (2013) demonstrated improved sustainable withdrawal rates by using the reverse mortgage term and tenure options in addition to using draws from the reverse mortgage line of credit.

Pfau (2016) evaluated six different retirement income strategies involving the use of a reverse mortgage. His research found that opening a line of credit early in retirement and using it systematically improved the probability of success and reduced failure rates compared to strategies that set up reverse mortgages as a last resort.

Despite research supporting the use of reverse mortgages, utilization of the strategy remains low. Less than 0.5 percent of U.S. households have a reverse mortgage, according to 2016 data from Strategic Business Insights.5 Davidoff, Gerhard, and Post (2017) examined the state of reverse mortgage usage and reverse mortgage literacy rates among seniors and suggested that the lack of a more robust reverse mortgage market could be in part due to misconceptions among the elderly. The research found that almost all respondents had heard about reverse mortgages but that the mean knowledge score was a 5.91 out of 13 points, or roughly a 45 percent knowledge score. The authors concluded that low reverse mortgage product-specific literacy could be a factor for low reverse mortgage demand.

Attitudes Toward Home Equity and Retirement

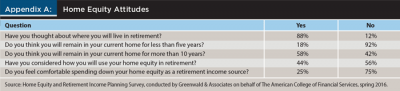

As stated earlier, one of the goals of The American College’s “Home Equity and Retirement Income Planning Survey” was to better understand how people nearing and in retirement felt about home equity and housing in retirement. The most basic retirement and housing question asked was: “Have you thought about where you will live in retirement?” Eighty-eight percent of the respondents stated that they have thought about where they will live, and 12 percent responded that they have not thought about where they would live in retirement. The existence of a financial adviser did have a slight impact on whether the individual had thought about where they would live in retirement, with 91 percent of those with advisers responding “yes,” compared to 84 percent without an adviser. (See the appendices for specific survey results and Table 1 for general statistical takeaways.)

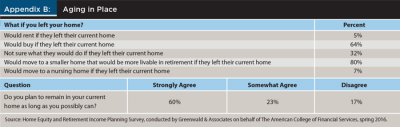

Aging in place. The majority of respondents indicated they wanted to age in place. When asked if they would want to live in their current home as long as possible, 60 percent of respondents stated that they strongly agreed with the statement, 23 percent somewhat agreed, and 17 percent disagreed. Additionally, 18 percent of respondents expected to be in their house for less than five years, while 58 percent of respondents expected to be in their current home for 10 or more years.

When asked where they would move if they left their current home, respondents showed a strong desire to continue being homeowners and living independently. Five percent of respondents replied that they planned to rent if they were to leave their current home, 64 percent expected to buy, and 32 percent were not sure what they would do. If they did decide to move, 80 percent of respondents wanted to move to a smaller home that would be more livable in retirement. Only 7 percent expected to move to a nursing home if they moved out of their home.

Using home equity in retirement. Survey respondents were also asked about incorporating home equity into their financial planning. Forty-four percent of respondents stated that they had considered how they would use home equity in retirement. Having a comprehensive written plan appeared to have an impact on considering the use of home equity in retirement; 52 percent of those with a written plan had considered using home equity in retirement, compared to 38 percent of those without a written comprehensive financial plan. This was statistically significant with a p-value < 0.0001.

The respondents were fairly confident that they were financially prepared for retirement, with 61 percent stating they were confident or extremely confident. However, when respondents were asked if they were confident that they will have enough income each year of retirement to cover their spending needs, there was a slight drop to 58 percent. However, there was not a significant difference between these two (61 percent and 58 percent) with a p-value of 0.159.

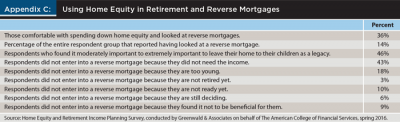

Most respondents (75 percent) did not feel comfortable spending down their home equity as a retirement income source. Comfort levels with using home equity as an income source were fairly consistent across most demographics, including age, investable assets, home equity, literacy scores, and the existence of a comprehensive plan. However, respondents who were comfortable spending down home equity (25 percent) were much more likely to consider using a reverse mortgage. Roughly 36 percent of those comfortable with spending down home equity looked at reverse mortgages, while only 14 percent of the entire respondent group reported having looked at a reverse mortgage. The proportion difference is significant, with a p-value <0.0001.

When running a logistic regression, the results suggest that those who are comfortable with spending down home equity are about 7.5 (odds ratio of 7.408) times more likely to have considered a reverse mortgage compared to those who are not comfortable spending down home equity in retirement. As such, the data showed that those who are not comfortable spending down home equity as an income source in retirement are unlikely to consider a reverse mortgage.

Adviser relationship. Sixty percent of respondents said they had an ongoing relationship with a financial adviser. Although 90 percent of respondents stated that they had a plan in place for the sources of their retirement income, only 49 percent of those with a plan reported having a comprehensive written retirement income plan in place. However, roughly 60 percent of those with a financial adviser had a comprehensive written plan. Running a logistic regression, the results suggest that the respondents with a financial adviser were roughly 3.5 (odds ratio of 3.429) times more likely to have a written plan than those without a financial adviser.

Reverse mortgage usage. Only one survey respondent had entered into a reverse mortgage. This is an area that could use additional research. For instance, it would be helpful to compare the knowledge levels and attitudes of those with reverse mortgages to those who did not consider or use a reverse mortgage. Little information could be gathered about this group due to the sample size. However, when asked about why the respondents decided not to enter into a reverse mortgage, 43 percent stated that they did not need the income. Eighteen percent of respondents said they were too young to enter into a reverse mortgage when they looked into it. Three percent responded that they did not enter into a reverse mortgage because they were not retired yet, 10 percent said they were not ready yet, and 6 percent said they were still deciding. Nine percent of those who considered a reverse mortgage found it not to be beneficial for them. Furthermore, 46 percent of the respondents stated that leaving their home to their children as a legacy goal was moderately to extremely important.

When asked whether they viewed a reverse mortgage as a positive tool that can improve retirement security, only 10 percent strongly agreed. About 52 percent either did not strongly agree or disagreed with the statement. Thirty-five percent had a negative view of reverse mortgages, and 2 percent had no feelings on the topic.

The individuals who scored a 70 percent or higher on the quiz were more likely to strongly agree that a reverse mortgage was a positive tool that could improve their retirement security than those who scored below a 70 percent, with a p-value < 0.001. As such, there is a strong indication that increased knowledge about reverse mortgages has a connection to a more positive view of reverse mortgages as a strategic retirement planning tool. However, even with the most knowledgeable respondents, positive views of reverse mortgages remained low with only 15 percent strongly agreeing that reverse mortgages are a positive retirement tool.

Reverse Mortgage Literacy

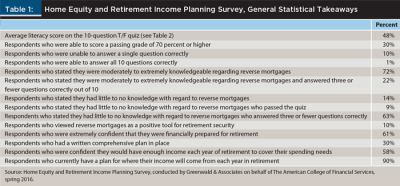

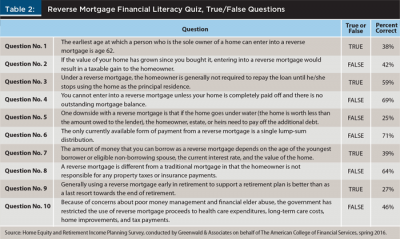

The average literacy score on the 10 questions in the true/false quiz was 48 percent correct. Only 30 percent scored a passing grade of 70 percent or higher, and 10 percent of the respondents were unable to answer a single question correctly. Just 1 percent of respondents answered all 10 questions correctly (see Table 2 for the quiz questions).

Respondents showed far more confidence in their own knowledge than demonstrated by the literacy quiz scores. For instance, 72 percent of respondents stated that they were moderately to extremely knowledgeable regarding reverse mortgages, but of the 72 percent that stated they were knowledgeable, roughly 22 percent of them answered just three or fewer questions correct out of 10. Fourteen percent of respondents admitted to having little to no knowledge about reverse mortgages and their perceived lack of knowledge showed in their reverse mortgage literacy scores, with only 9 percent posting a passing score, and 63 percent of this subset of respondents answering three or fewer questions correctly.

Perceived knowledge regarding reverse mortgages was connected to actual knowledge. Using a linear regression, results suggest that those with a high perceived knowledge scored about 19 percentage points (coefficient of 0.187) higher on the knowledge questions than those with low perceived knowledge. This group was also much less likely to have a written comprehensive plan in place; 30 percent had a comprehensive written plan while 70 percent did not.

Overall, respondents did not demonstrate a high level of comprehension of the features of reverse mortgages, however, some areas were better understood than others. The most misunderstood aspect of reverse mortgages was question No. 5, which asked the respondents about the non-recourse aspect of a reverse mortgage. According to the U.S. Department of Housing and Urban Development, the reverse mortgage HECM is a non-recourse loan, which means “that the HECM borrower (or his or her estate) will never owe more than the loan balance or the value of the property, whichever is less, and no assets other than the home must be used to repay the debt” (HUD Handbook, page 1).6 However, only 25 percent of respondents knew that the heirs or homeowner did not have to pay off the additional reverse mortgage debt if the house was not enough to cover the amount.

The second most misunderstood question was about when a homeowner should consider using a reverse mortgage. Traditionally, reverse mortgages were often thought of as a financial last resort and respondents expressed this sentiment. Only 27 percent stated that, in general, it was better to use a reverse mortgage earlier in retirement as opposed to being used as a last resort.

Research has demonstrated that reverse mortgages are often more effective if used strategically early in retirement rather than being used as a last resort when all other assets have been depleted (Pfeiffer, Schaal, and Salter 2014). FINRA previously published an investor alert that reverse mortgages should be used as a “last resort” but, in 2014, removed the language from its statements.7 And in early 2015, new requirements were put in place requiring the mortgagee to evaluate a potential mortgagor’s ability to meet his or her financial obligations through a financial assessment.8 Due to the heightened financial assessment requirements, it is likely that many individuals seeking to use a reverse mortgage as a true last resort will no longer qualify for the program.

The third most misunderstood question was about when a homeowner could enter into a reverse mortgage. Any homeowner or eligible borrower needs to be age 62 or older. Although it might appear to be a fairly simple and technical aspect of reverse mortgages, only 38 percent of respondents knew the answer. Respondents did not know when to use reverse mortgages most effectively or when they could even enter into a reverse mortgage. Furthermore, only 46 percent of respondents knew that reverse mortgage proceeds could be used for a variety of retirement expenditures and that they were not limited to just long-term care and taxes. The highest correct response rate was about how a homeowner could have reverse mortgages proceeds distributed. Most respondents (71 percent) stated that a lump sum distribution was not the only form of reverse mortgage payout. In fact, reverse mortgage distributions can come in a variety of payment plans, including a tenure option, term payments, a line of credit, and a lump sum amount.

When the respondents were questioned about how the proceeds from a reverse mortgage were calculated, 39 percent answered correctly. Many factors go into calculating the amount that a borrower can receive from a reverse mortgage. That amount is based on an amount referred to as the principal limit, which is calculated based on “the age of the youngest borrower, the expected average mortgage interest rate, and the maximum claim amount” (HUD Handbook, page 2).

In a related question, respondents performed much better; 69 percent of respondents correctly answered that a homeowner could engage in a reverse mortgage even if there was an outstanding, traditional forward mortgage on the home. Although a lien or loan against the house will impact the amount a homeowner can borrow from a reverse mortgage, if the debt is less than the principal limit, the homeowner may qualify for a reverse mortgage.

Most respondents did not understand the taxes related to the loan. Only 42 percent of the respondents knew that borrowing money through a reverse mortgage would not create a taxable income event for the homeowner at the time of the loan. However, 64 percent knew that the homeowner is not relieved of the responsibility of paying property taxes and insurance premiums on the home.

Fifty-nine percent of respondents understood when a reverse mortgage must be repaid. A reverse mortgage is “repaid in one payment, after the death of the borrower, or when the borrower no longer occupies the property as a principal residence” (HUD Handbook, page 1). Once the borrower stops using the home as the principal residence, the reverse mortgage becomes due in full, including any interest that has accumulated.

Implications for Advisers

The survey brought to light several takeaways for financial advisers. First, respondents wanted to age in place and stay in their home for as long as possible. Second, most respondents had not thought about using home equity in retirement. Third, respondents did not demonstrate a high level of knowledge about reverse mortgages. And finally, the existence of a financial adviser relationship had little to no impact on a respondent’s reverse mortgage knowledge.

There was no statistically significant difference on total knowledge between those with an adviser and those without an adviser (p-value of 0.95). There was no statistically significant difference in whether a respondent had a high knowledge score (70 percent or better) or if he or she had an adviser or not (p = 0.132). Additionally, only 14 percent of those with an adviser stated that they had considered a reverse mortgage, compared to 15 percent of those without. There was also not a statistical significance between the existence of a relationship with a financial adviser and the likelihood of the respondent to have considered a reverse mortgage compared to those without a financial adviser. This brings forth an important question: how involved should a financial adviser be with his or her client’s home equity planning in retirement?

The reality is that for the average American couple at age 65, home equity is their largest asset, almost double the size of any other investable savings they have accumulated. Prior research, discussed earlier, has demonstrated the value of incorporating reverse mortgages into retirement income plans. It seems prudent for a financial adviser to use any resources available to improve a client’s retirement. However, the survey results shared here show: the use of reverse mortgages is extremely low; interest in reverse mortgages is low; respondents were very suspicious about the benefits of reverse mortgages; and reverse mortgages are widely misunderstood. Furthermore, there was no evidence that financial advisers have widely embraced the strategy since usage, literacy, and home equity planning were not significantly impacted by the existence of a financial adviser relationship.

Integrating Home Equity into a Retirement Income Plan

What happens if an adviser does decide to embrace the idea and incorporate reverse mortgages and home equity into the planning process? First, the adviser needs to understand that his or her clients likely have not thought about using home equity as a retirement income option and will not likely have a well-informed or positive position on reverse mortgages. The adviser will likely have to educate the client on the effective uses of reverse mortgages. Advisers may also face compensation and compliance hurdles.

However, home equity is one of the client’s largest assets and it can be effectively used to improve a retirement income plan. Basic housing decisions like where to live are crucial to a retirement plan; it follows that to better assist clients with their retirement planning, home equity should be incorporated into the plan. This includes looking at potential strategies to turn home equity into income through a reverse mortgage. Of course, a reverse mortgage will not be suitable or in the best interests of every client.

To properly use reverse mortgages and home equity as part of a retirement income plan, the adviser must understand the client’s situation, goals, needs, and retirement risks. This starts by gathering financial and legal information about the client’s home including its value, any outstanding debt, and how it is titled. It is then prudent for the adviser to ask these five basic questions to better understand the client’s housing situation in retirement and if home equity is a potential beneficial income source:

- Where do you want to live in retirement?

- How long do you want to live in your current home?

- Do you feel comfortable using home equity as a strategic retirement income source?

- Do you want to use your home to fund your long-term care expenses?

- Do you want to leave your home to your heirs?

Currently, reverse mortgages have four distribution options, each of which have different uses. Lump sum distributions can be used to pay off an existing mortgage, purchase a new home by entering into a HECM for purchase, or for general cash flow needs. For instance, a client with an existing mortgage might want to use a HECM to pay off their existing mortgage in order to ease their monthly cash flow as the HECM does not require monthly payments of principal and interest.

A reverse mortgage can be taken as tenure payment, which functions like an annuity by making fixed monthly payments to the borrower as long as he or she continues to live in the home. This can be a way to continue living in the home but at the same time create a monthly stream of cash from the home equity.

Then there are term payments, which can be used to build income bridges. For instance, some advisers are using the term payment with an eight-year term to build a bridge from when a client retires at age 62 until age 70.

Lastly, a reverse mortgage does not require an immediate withdrawal of home equity. Instead, you can set up a line of credit that you only tap into when needed. This line of credit can be a good way to build a non-market correlated income stream to use after down market years. However, remember that most of the more effective reverse mortgage strategies are still based off the assumption that the client wants to continue living in the house for many years.

If a client does not want to age in place, a reverse mortgage might not be the ideal solution. If the person plans to relocate in a few years or owes too much money on his or her home, the benefits of using a reverse mortgage could be reduced. The adviser needs to understand how comfortable the client is with using his or her home as an income stream. Many of the survey respondents were not comfortable with the idea. Even after some education on the topic, a client might not feel comfortable using home equity for retirement income. The adviser must be prepared to educate the client and make sure to use the appropriate strategy for each client’s specific situation, goals, and needs.

Endnotes

- See “Seniors’ Incomes in 47 States Don’t Go Far Enough” available at bankrate.com/finance/retirement/study-seniors-incomes-dont-go-far-enough.aspx.

- See “The Current State of Retirement: A Compendium of Findings about American Retirees” available at transamericacenter.org/docs/default-source/retirees-survey/tcrs2016_sr_retiree_compendium.pdf.

- See the U.S. Department of Health and Human Services’ “Profile of Older Americans 2015” available at aoa.acl.gov/aging_statistics/profile/2015/docs/2015-Profile.pdf.

- See the annual HECM endorsement chart available at nrmlaonline.org/2016/10/04/annual-hecm-endorsement-chart.

- See “MacroMonitor Data—Potential Reverse-Mortgage Households” August, 2016, available at strategicbusinessinsights.com/cfd/segmentsums.shtml.

- Available at portal.hud.gov/hudportal/documents/huddoc?id=42351c1HSGH.pdf.

- See “Reverse Mortgages: Avoiding a Reversal of Fortune” available at finra.org/investors/alerts/reverse-mortgages-avoiding-reversal-fortune.

- See “HECM Financial Assessment and Property Charge Guide” available at portal.hud.gov/hudportal/documents/huddoc?id=14-22ml-atch2.pdf.

References

Blumenthal, Robin Goldwyn. 2015. “A Debate on Improving Ways to Fund Retirement.” Barron’s. Posted Sept. 12, available at barrons.com/articles/improving-ways-to-fund-retirement-1442034508.

Davidoff, Thomas, Patrick Gerhard, Thomas Post. 2017. “Reverse Mortgages: What Homeowners (Don’t) Know and How It Matters.” Journal of Economic Behavior and Organization 133 (1): 151–171.

Hultquist, Dan. 2017. Understanding Reverse: Answers to Common Questions—Simplifying the New Reverse Mortgage. CreateSpace Independent Publishing Platform.

Pfau, Wade D. 2016. “Incorporating Home Equity into a Retirement Income Strategy.” Journal of Financial Planning 29 (4): 41–49.

Pfeiffer, Shaun, C. Angus Schaal, and John Salter. 2014. “HECM Reverse Mortgages: Now or Last Resort?” Journal of Financial Planning 27 (5): 44–51.

Sacks, Barry H., and Stephen R. Sacks. 2012. “Reversing the Conventional Wisdom: Using Home Equity to Supplement Retirement Income.” Journal of Financial Planning 25 (2): 43–52.

Salter, John R., Shaun A. Pfeiffer, and Harold R. Evensky. 2012. “Standby Reverse Mortgages: A Risk Management Tool for Retirement Distributions.” Journal of Financial Planning 25 (8): 40–48.

VanDerhei, Jack. 2015. “Retirement Savings Shortfalls: Evidence from EBRI’s Retirement Security Projection Model.” EBRI Issue Brief 410.

Wagner, Gerald C. 2013. “The 6.0 Percent Rule.” Journal of Financial Planning 26 (12): 46–59.

Citation

Hopkins, Jamie. 2017. “The Effect of Low Reverse Mortgage Literacy on Usage of Home Equity in Retirement Income Plans.” Journal of Financial Planning 30 (5): 44–52.